What’s ahead for the economy in 2022?

Policymakers aim to simultaneously tame inflation and extend the business cycle. Meanwhile, Covid-related uncertainty remains.

So many moving parts. That’s what makes economic forecasting traditionally challenging. And the task is even more daunting for 2022, due to the added uncertainty of an unprecedented global pandemic. But while predictions are difficult, the central questions around the economy in the new year — the ones business executives need to monitor in the months ahead — are clear:

- Will policymakers pull the right levers to successfully address Covid-19’s impact on the labor markets and supply chain disruptions and foster sustainable growth while combating high inflation levels? Will they be able to bring the economy in for a soft landing?

- And, importantly, will Covid-19 uncertainties begin to lift and provide a big assist in returning the economy back to normal?

This outcome seems doable. It just might not happen right away, and adverse market forces can delay progress.

In fact, for 2022, we envision a tale of two halves. It may take some time for policy initiatives to produce the desired results, so don’t expect a major righting of the ship in the first half of the year. But in the U.S., we expect a meaningful decline in inflation over the course of the year and a return to sustainable trend-like growth.

Conditions at the Outset of the Year

The 2021 economic picture was dominated by pandemic developments. The vaccine rollout provided some return to normalcy as businesses reopened. In the U.S., a hefty dose of government stimulus lifted income well above prior prevailing trends and helped push wages up along with prices. The U.S. economy posted some of the strongest quarterly growth levels in history, with GDP growth up more than 5%. At the same time, high energy prices and shortages induced by supply bottlenecks helped drive the consumer price index near 7%. Now, however, the U.S. economy is moving from a boom phase after the reopening toward a moderating period. Depending on the policy prescription, we could be heading for what may feel like a mid-cycle slowdown in the second half of 2022.

Historically speaking, this is very typical of sharp-growth periods turned more muted. In many ways, Covid seems to be impacting the economy in a very similar way to what the country has seen from past major conflicts that have impacted production and reduced supplies with a commensurate shift in aggregate demand.

How will 2022 play out? We view the consensus view of nearly 4% GDP growth for 2022 to be higher than what will ultimately be realized, and we expect inflation to initially stay high.

Getting Inflation Back Under Control

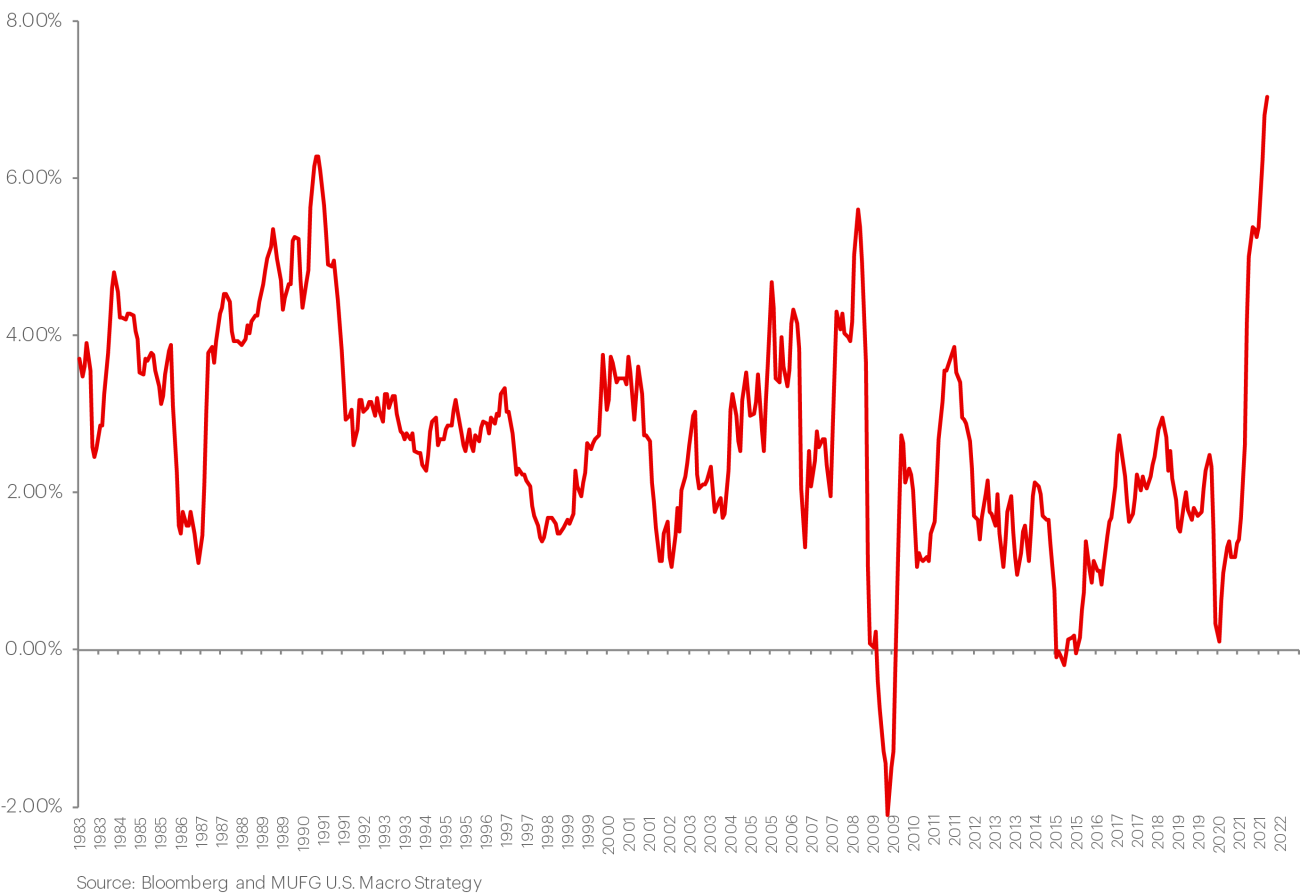

Inflation Reaches 40-Year High

Historical YoY Consumer Price Index (CPI)

Entering 2022, inflation is the No. 1 economic issue and constitutes the biggest unknown. The speed at which inflation can be driven down toward more historically typical levels will depend on actions taken by the Federal Reserve, which has pivoted to an increasingly hawkish stance on inflation fighting.

We anticipate a front-loaded Fed tightening cycle this year — a minimum of three hikes in its benchmark federal funds rate with the potential for more if either the Fed does not start shrinking its balance sheet soon, as we expect sometime early this year, and/or if inflation proves to be even more persistent than what we expect.

Inflation will likely peak in the first half of the year. Overall, 2022 should be another year of elevated headline inflation, albeit heading towards levels lower than last year, on average.

Temporary shocks are causing headline inflation to be higher than normal, and those shocks should start to wear off. However, even with our best case of higher inflation that eventually recedes in the second half, we’re forecasting headline inflation rates in the mid to high 3% range. That’s better than in 2021 but still well above the historical annual average — something in excess of 2%.

Prospects for a More Stable Supply Chain

One reason we see inflation moderating in the second half is the continuing improvement we expect in the supply chain during the course of 2022.

This is one of those ailments that will require the passage of time to determine if things are improving. If Covid subsides as the omicron variant works its way through the population and vaccination levels and other protective measures take hold, reduced concerns over Covid-related impacts should get more laborers back to work and reduce supply disruptions.

At the same time, efforts by local and federal authorities to open ports and promote reshoring initiatives should facilitate a greater flow of goods.

Supply chain bottlenecks should clear up in the second half, leading to the supply of available goods starting to exceed demand. There is a risk that as the economy normalizes in a post-Covid world, we could see an inventory glut in the years ahead.

Moderating Growth

In the first half, the economy will continue to be propelled by the momentum of the past year, much of it driven by pandemic-related government stimulus efforts and the reopening efforts.

In the second half, however, we expect a sharper deceleration due to upcoming monetary tightening and fiscal drag. While the Fed is forecasting 4% GDP growth for 2022, and the consensus lines up at 3.9%, we are projecting a more moderate growth rate.

A Comeback for the U.S. Labor Force?

The U.S. economy started 2022 with strong momentum, as the jobs market continued to show improvement with healthy wage gains and a record number of job openings (more than 11 million).

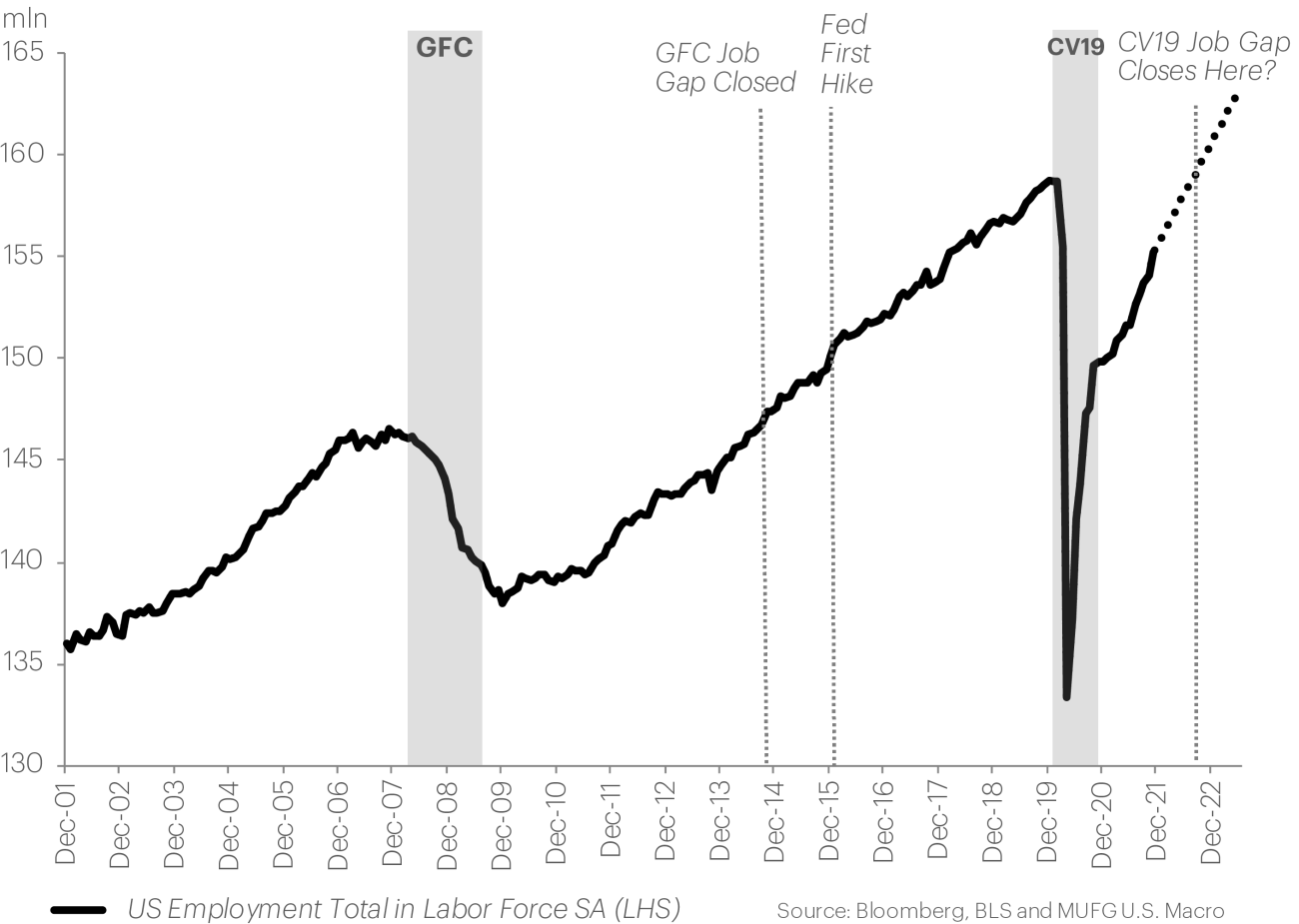

From an historical perspective, the jobs recovery following a sharp decline in the total labor force after the pandemic’s onset has been lightning fast.

It took roughly seven years to regain all the jobs lost following the financial crisis of 2007-2008. The pandemic-produced decline in jobs was much sharper due to forced workplace closings, but the rebound is proving to be equally dramatic.

At the current average pace of job growth, the gap created by Covid-related job losses should close sometime in the late summer of 2022 (see chart). If Covid-related concerns in the labor force ease further, one risk of returning to a fully functioning economy is that an excess in labor supply is built in the jobs market. If so that could ease the labor shortage issues as well.

REGAINING LOST JOBS AFTER COVID’S ONSET

Gap closing faster than after the Great Financial Crisis

Impact of Global Economic Trends on the U.S.

Of course, everything doesn’t ride on the Fed and what happens within U.S. borders. The U.S. is not an island. The health of the global economy is another important factor that will impact U.S. economic trends in 2022.

Of paramount importance will be how countries around the world perform as they reopen fully. Developments to keep an eye on include vaccination levels worldwide, related levels of Covid infections, and the speed at which other key countries are able to maintain and further open up their economies. Global economic growth will have an impact on U.S. growth prospects.

Another factor worth monitoring: Are other countries raising interest rates? If so, the Fed won’t have to hike as much in 2022 and that can go a long way toward ensuring the U.S. dollar doesn’t get too strong. However, a global synchronized rise in interest rates could also tighten financial conditions more broadly.

Making the Right Moves and Avoiding Major Risks

Even in the best of times, central banks must execute like chess masters. But in 2022, with an ongoing pandemic still in the background, there are more pieces on the board to take into account. Making the right moves becomes all the more difficult in this environment given the inflation risks. But it’s their policies and actions that will make a huge difference in the coming year. In the U.S., we’ll be watching for answers to these questions:

- Can policymakers handle the inflation problem without decelerating the economy to such an extent that we fall into a period of shallow growth or even a stalling out of the economy?

- Can they maneuver us back into a Goldilocks scenario of sustainable trend-like growth and more traditional inflation levels?

- We’ve never had to deal with a massive inflation problem at a time of peak valuations in various sectors of the financial markets. Will policymakers be able to tame inflation without dragging down the markets and shortening the business cycle?

There are some major risks to our outlook for the economy in 2022.

If the Fed tightens enough to trigger a material rise in real rates — one of the factors that could help lead to tighter financial conditions — the risk is that the economy quickly falls back into pre-Covid stagnation. The worst case scenario is that the business cycle ends up being shortened due to Fed tightening policy.

Meanwhile, this does not account for the unforeseen — such as the pandemic not lifting as soon as most are expecting, further restricting growth, or some other geopolitical events that could derail economic activity.

Learn More

Please contact your treasury relationship manager.