In the Long Shadow of COVID, What’s Next?

The world has come a long way since the depths of the COVID-19 pandemic last year. Of course, the pandemic is still far from over, and new strains, such as the Delta variant, still pose risks to a full economic recovery. But with the advent of vaccines and continued help from governments and central banks to support the capital markets, businesses have reopened, employees are gradually returning to the office, and the credit environment is improving. Certain economic activities have partially recovered, fully rebounded or reached historic highs; others have been structurally altered.

At MUFG, we assembled a host of our prominent thinkers—lead bankers, analysts and strategists—to provide a rough sketch of where they see the next 6–12 months. They include Tom Joyce, Head of Capital Markets Strategy; Elizabeth Everett, Head of Middle Market Healthcare; Andreas Dirnagl, Global Head of Healthcare Research; George Goncalves, Head of U.S. Macro Strategy; Leanne Rakowitz, Head of ESG Coverage; Amanda Kavanaugh, Head of Sustainable Finance Capital Markets; and Allison Valvano, Vice President of Healthcare Banking.

We invite you to explore their impressions here.

MUFG Americas

1251 Avenue of the Americas

New York, NY, 10020-1104, United States

Strong Capital Markets—Despite Elevated Risks

Head of Capital Markets Strategy Tom Joyce points to robust capital-markets activity and economic growth well above historical trends, fueled by extraordinary Fed and monetary-policy accommodation. He says the pace of growth may decelerate to more moderate levels and cites certain elevated macro risks, though his overall prognosis is squarely positive.

By Tom Joyce

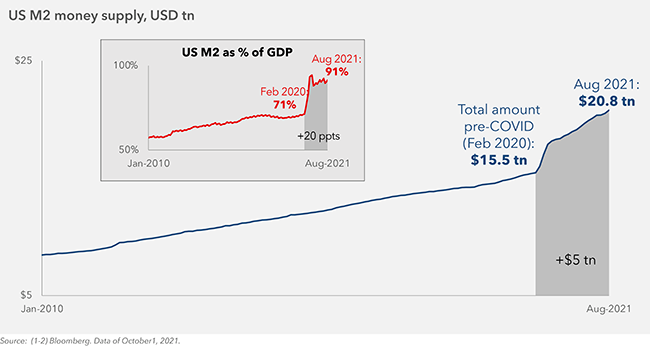

In retrospect, the reversal of fortunes from 18 months ago is nothing short of remarkable. Much like on the eve of the 2008 financial crisis, no one who followed the markets in March of 2020 will likely forget the gathering storm as financial assets across the board were being liquidated for cash, equities declined sharply, credit markets seized up and businesses shuttered amid lockdowns and social distancing. Yet here we are, after what seems like a year in fast forward. Although U.S. Federal Reserve accommodation is past its peak, monetary policy remains extraordinarily easy, with M2—a measure of the money supply that includes cash, checking deposits, and other assets easily convertible to cash—currently $5 trillion above its pre-COVID levels. In short, the financial markets are experiencing excess liquidity at record levels (Exhibit 1).

Exhibit 1: Monetary policy is extraordinarily accommodative

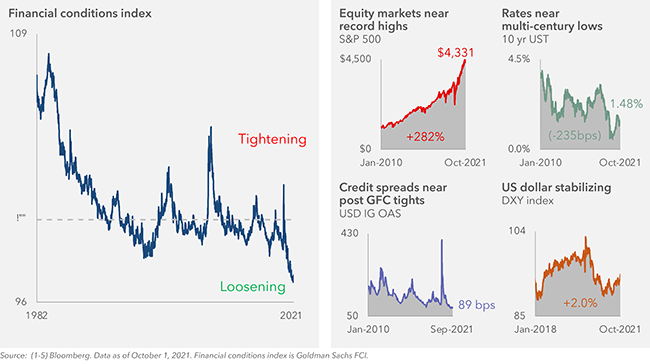

What’s more, even as the Fed pivots its policy toward a more tightening stance, financial market conditions remain at historically easy levels with equities near all-time highs, rates at multicentury lows, credit spreads tight, and the U.S. dollar index stabilizing at more accommodative levels (Exhibit 2).

Exhibit 2: Financial conditions remain easy

Equally impressive, global growth this year is expected to be two to three times its “normal” rate (which we define as its long-term average). It’s worth noting that growth this year likely peaked for the United States in the second quarter and for the world in the third quarter—and full-year estimates declined of late (Exhibit 3). While the Delta variant adds additional risk to gross domestic product (GDP) numbers, U.S. and global economic growth are still high relative to historical standards—and we believe they will remain elevated (though decelerating) in 2022 as well.

Exhibit 3: GDP growth expectations have peaked and slightly declined, yet remain well above historical averages

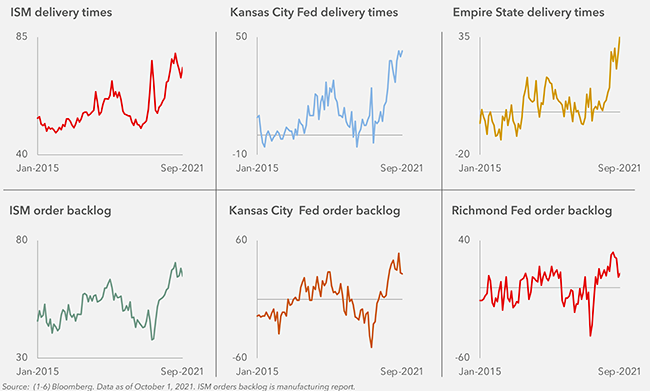

It appears that inflationary pressures and supply-chain dislocations will continue well into 2022, and they are already showing signs of adversely impacting economic growth. And although the pricing pressures created by persistent labor shortages, shipping delays, production bottlenecks and higher commodity prices are likely past their peak in aggregate, we believe they will remain elevated into 2022 (Exhibits 4-5).

Exhibit 4: Supply chain metrics indicate longer delivery times and elevated backlogs

Exhibit 5: Supply-chain disruptions have pushed up prices

Tom Joyce

Head of Capital Markets Strategy

What Living With COVID Means for Healthcare

Our Healthcare Banking team cites the traditional drivers that, in their view, make the healthcare industry relatively stable, including an aging global demographic, the prevalence of chronic diseases and relatively inelastic demand. The team’s conviction in this thesis is only strengthened by the industry’s performance in face of a global pandemic. And although there was some variability in the effects of COVID-19 on different healthcare sectors, the industry as a whole is expected to show continuing solid financial performance, according to Elizabeth Everett, Head of Middle Market Healthcare; Andreas Dirnagl, Global Head of Healthcare Research; and Allison Valvano, Vice President of Healthcare Banking.

By Elizabeth Everett, Andreas Dirnagl, and Allison Valvano

From a macroeconomic perspective, healthcare is considered a defensive sector because it is comparatively non-cyclical: It offers products and services that consumers need and continue to consume in most economic environments.

Granted, the healthcare industry itself is diverse and has been affected in uneven ways by the pandemic. Last year, for example, social distancing had accelerated the business of pharmaceutical companies because of “shelter-in-place” orders, which resulted in the extension of medication prescriptions to last for prolonged stays at home. Pharma companies with consumer-products businesses benefited from this trend as sales of over-the-counter drugs and household products (such as cleaning agents) went up. On the other hand, the delays and cancellations of non-essential surgeries and various other procedures challenged many hospitals financially and impinged on their revenues.

Yet moving forward—with some variability among sub-sectors—we expect the healthcare industry in aggregate to continue exhibiting strong financial performance.

From Pandemic to Endemic

The backdrop for our expectation is, not surprisingly, COVID-19, which will continue to preoccupy the industry in evolving ways.

In our view, what began as a pandemic will become endemic, with vaccinated people learning to “live with COVID” as a regularly occurring disease over the next one to two years in the industrialized world and perhaps five or more years in emerging and undeveloped economies. The rates and timing of transmissions and outbreaks are likely to vary by geography, but we believe they will be regionally contained.

Implications for Medtech, Healthcare Services and Pharma

This prolonged, lingering public health risk bears implications for medtech companies, which develop technologies, supplies and capital equipment used in a care setting, such as medical and surgical devices and instruments, diagnostic tests, implant materials, biomaterials and disposables. It will also affect the healthcare services sector, which consists of medical professionals, organizations such as hospitals, and workers who provide medical care to those in need. We expect both sectors to experience continuing levels of uncertainty, with periodic localized disruptions.

Companies whose financial performance was boosted by the pandemic (including diagnostic laboratories, healthcare staffing, hospital equipment and manufacturers of personal protective equipment such as gloves and masks) should continue to see growth and opportunity, albeit at a reduced rate. Organizations dependent for revenue on elective procedures (i.e., any surgery that must be done but that need not be performed immediately, such as the kind offered by dentistry practices and other surgery providers) will likely experience periodic disruptions, though they are unlikely to approach the early days of the pandemic last year in frequency and scale.

We anticipate COVID testing services to remain in strong demand worldwide, driven in part by office-reentry initiatives. Of note, such testing is now being incorporated into urgent care and pre-surgical protocols, similar to testing for such other endemic viruses as the flu.

Since the majority of the world’s population has not yet received its first dose of the COVID‑19 vaccine, we expect more widespread vaccine mandates and booster shots among populations of advanced economies, which should benefit pharmaceutical companies that manufacture vaccines. We also foresee continued growth for developers of COVID treatments and medications.

Smaller Crowds

Finally, from a public-health safety perspective, we expect crowd volumes at large-group activities and events, business travel and entertainment venues to remain up to 20% below pre‑pandemic levels in the medium and perhaps long term.

Elizabeth Everett

Head of Middle Market Healthcare

Andreas Dirnagl

Global Head of Healthcare Research

Alison Valvano

Vice President of Healthcare Banking

U.S. Rates: at a Critical Crossroads

According to Head of U.S. Macro Strategy George Goncalves, the markets for rates (i.e., government bonds and related securities) are a seismic gauge of the direction and health of the economy and capital markets at large. If the economy continues to perform well in 2022 and the bond market does not realign itself with higher long-term interest rates, we could witness an additional buildup of leverage and potentially other systemic imbalances. Yet it could also imply a signal from the bond market that the current rate of economic growth may not be sustainable.

By George Goncalves

A move toward lower long-term interest rates on government bonds has usually occurred when the market was trying to tell us something—that growth was about to falter, inflation was about to decline, or both. And it would normally lead the central bank to cut short-term rates in an effort to boost aggregate demand and prop up the economy.

However, at this juncture, most forecasts do not suggest that the economy is headed toward a protracted slowdown, but rather that economic growth will level off from its peak and revert to “trend growth”—its long-run average rate—with commensurate moderation in the rate of inflation.

So why are long-term rates on government bonds so low?

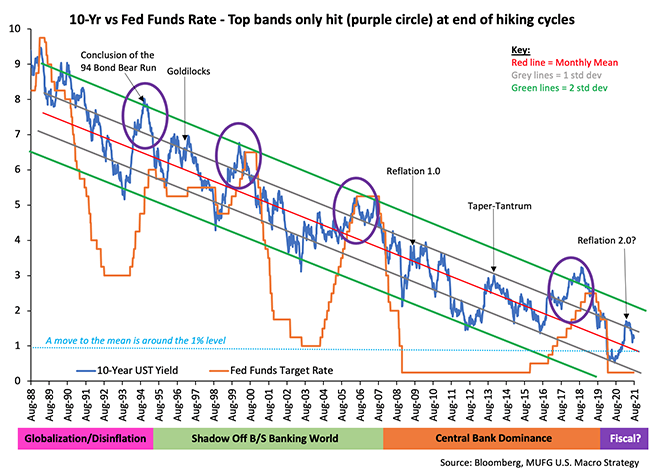

As they say in the bond market, it’s always relative. From a 30,000-foot view—and as we can see in Exhibit 4—rates have been on a progressive move toward lower lows and lower highs since the 1980s. In other words, each new low since that time was followed by a subsequent lower high (i.e., a level not as high as the one preceding it). This multi-decade decline in interest rates has been a reoccurring phenomenon, even during periods of rate-hiking campaigns by the Federal Reserve, and it suggests that the gravitational pull toward lower rates is more of a structural market feature than an anomaly. Yet it doesn’t stop markets from attempting to price in higher rates during a recovery phase.

Exhibit 4: The bond market has been experiencing a multi-decade decline in rate levels

At the start of the second quarter of this year, our interest-rate forecasts were a bit unconventional. We initially believed rates would decline into the summer before rising back up to roughly the same level by year-end. Although we were mostly right about the declining part, we did not expect rates to go well below the levels they have already hit on their way down.

As things stand now, we believe this latest downward trend in long-term rates—call it the “2021 Summer Rates Rally”—may have gone too far in view of the more constructive outlook we have about the economy in the months ahead.

It appears we’re at a critical crossroads, with the Fed appearing ready to begin the process of removing excess accommodation by tapering its bond-purchasing program, known as “quantitative easing” (QE). If long-term rates do not rise after such a step—or if they continue their decline—then it might be the bond market’s way of signaling that the current rate of economic growth is unsustainable.

Either way, we’re keeping a watchful eye.

George Goncalves

Head of U.S. Macro Strategy

The Post-Pandemic Landscape for ESG

The past 18 months have seen seismic change—economically, socially, politically and culturally— that has catalyzed the adoption of environmental, social and governance (ESG) considerations in the financial markets, according to our ESG Origination and Client Coverage team. Head of ESG Coverage Leanne Rakowitz and Head of Sustainable Finance Capital Markets Amanda Kavanaugh explain that investors are increasingly integrating ESG factors into investment analysis and borrowers are considering them in business and capital plans. The team expects continued focus on ESG in a post-pandemic world with collaboration, as well as regulation, advancing ESG‑related standards.

By Leanne Rakowitz and Amanda Kavanaugh

The first half of 2020 saw massive social demonstrations and the arrival of the COVID pandemic, both of which shone a spotlight on inequalities in American society. Additionally, weather-driven disasters ravaged many communities throughout the globe, brought further challenges to vulnerable populations during the pandemic, and influenced public sentiment; such extreme weather is becoming increasingly frequent with climate change, as detailed in the latest IPCC report. These and other events over the past year and a half highlighted our interconnectivity, such as our reliance on essential workers, the fragility of global supply chains, and the degree to which we are affected by others’ approaches to the pandemic, the environment and cybersecurity.

The Response From Investors

With eyes wide open to our interdependence and the potential high costs of mismanaging environmental, social and governance matters, the shift in emphasis on ESG in finance has been profound and swift. ESG-focused companies and funds generally outperformed during the pandemic, and capital has flowed to investment managers that apply an ESG lens. This investor interest, as well as fiduciary responsibility and sector trends, has prompted more managers to integrate ESG into investment analysis and to urge companies to address ESG risks and opportunities. As a result, the 2021 proxy season was the most active yet, with special attention on climate, DE&I (diversity, equity, and inclusion), and political spending. To help leverage their collective power and advance sustainable investing objectives, investors have formed new alliances or joined existing ones, like Principles for Responsible Investing (PRI) or Climate Action 100+. Notably, the Net Zero Asset Managers Initiative, formed less than a year ago in December 2020, currently has 128 signatories representing $43 trillion in assets under management.

Government, Regulator and Ngo Activity

The past 18 months has been a period of tremendous progress by non-governmental organizations (NGOs), regulators, and governments. Last fall, the major sustainability reporting standards-setters provided a vision for a comprehensive reporting framework and their future collaboration. The International Financial Reporting Standards Foundation (IFRS) is now working to form an International Sustainability Standards Board (ISSB) to establish global sustainability reporting standards that will replace voluntary ones, with hopes it will be formalized ahead of the United Nations Climate Change Conference of the Parties (COP 26) in November. This work will help address one of the largest obstacles for ESG in finance – the lack of consistent, comparable disclosures from issuers.

Government and regulatory response on ESG has been equally impressive, focused on pandemic-related stimulus to progress environmental and/or social objectives, disclosure requirements, and financial regulation to address systemic risks. Currently, we are still awaiting confirmation and much of the detail on these topics in the U.S. Globally, with respect to carbon emissions, current government pledges still fall short of what is needed to limit global warming to 1.5 degrees Celsius, but the gap narrowed from 18 months ago, and interest remains strong.

The Response From Business

In response to investor and regulatory attention, corporations are re-evaluating their strategies and risk management practices, providing more information to the market, and announcing sustainability goals. Many are aligning their sustainability plans with the United Nations’ Sustainable Development Goals (SDGs), which offers a form of categorization, and adhering to more of the voluntary frameworks in their reporting. They are also tapping into the rapidly growing sustainable financing market.

The Sustainable Financing Market

The sustainable financing markets have been experiencing a strong acceleration. Green, social, sustainability and sustainability-linked bond sales so far this year total $794 billion globally compared with about $480 billion in all of 2020, according to data compiled by Bloomberg. On the loans side, green, social, and sustainability-linked loans accounted for more than $500 million year-to-date.

In an effort to encourage further growth, ICMA and LSTA, in partnership with other regional loan market associations, have provided and updated guidance for standardization and best practices. Overall, we are seeing sustainable issuances across a wider range of sectors and more labelled issuances for renewable energy project finance, as investors become more focused on the impact of their capital. For sustainability-linked issuances, emissions and diversity key performance indicators are generally well-received, given the focus on these topics at this moment. These debt products are a useful tool for corporates to broadcast their sustainability initiatives and tap into pockets of dedicated ESG funds.

Outlook

In conclusion, we believe the ESG imperative is here to stay and will be driven by demands from investors, regulators, customers, and other stakeholders. We anticipate greater transparency in corporate data and reporting, and increased corporate engagement and collaboration to manage sustainability goals across entire value chains. We also expect heightened and sustained focus on corporate accountability and scrutiny on the role of finance in this ecosystem. The ultimate outcome of this evolution, in our view, will be the full normalization

Leanne Rakowitz

Head of ESG Coverage

Amanda Kavanaugh

Head of Sustainable Finance

Capital Markets